Background

United States shareholders of controlled foreign corporations (“CFCs”) are required to include certain forms of passive income in their taxable income. This is referred to as “subpart F income” by reference to its position in the Internal Revenue Code. Subpart F income is includable as ordinary income. Until the enactment of recent tax reform legislation, if income of a CFC was not subpart F income, the U.S. shareholders did not have to include it when calculating their income for the current year and the tax was effectively deferred. This has changed with the adoption of the Global Intangible Low-Taxed Income (“GILTI”) regime, as part of the Tax Cuts and Jobs Act, which will require non-subpart F income to be taxed currently but at a lower rate than regular income. We will turn to that at the end of this note. Prior to the enactment of the Tax Cuts and Jobs Act, on December 19, 2017, the Treasury and the Internal Revenue Service proposed regulations under sections 446, 988 and 954 (the “Proposed Regulations”) that favorably impact the treatment of foreign currency hedges of the activities of a CFC, some of which we will describe below.

The Business Needs Exclusion

Treasurers often hedge foreign currency risk related to their business operations. For example, if a company expects to incur a euro-denominated liability, it might hedge this liability by buying a euro forward. When a CFC generates currency gains in excess of currency losses, the net amount is usually considered foreign personal holding company income (“FPHCI”) and is included in subpart F income (i.e., is currently included in the income of the owner of the CFC’s income). There is an exception for transactions entered into in the ordinary course of the taxpayer’s business, including items that hedge those transactions – that is, “bona fide hedges” – that generate currency gains but not other types of subpart F income. The exception for currency gain or loss on the underlying transaction and on hedges of those transactions is referred to as the “business needs exclusion,” and any foreign currency gain on the hedges will not be included in subpart F income, as long as none of the underlying transactions being hedged generate subpart F income. The result of failing the requirement that none of the gain be subpart F income is that all of the gain is included in subpart F income. Because of this, it is said that there is a “cliff effect” in failing the requirement. For example, where a CFC hedges an aggregation of subpart F and non-subpart F exposures, the hedge may not be a bona fide hedge – i.e., the entire amount of gain realized on the hedge will be subpart F income.

A second situation many treasurers will find familiar is the case in which a CFC serves as a treasury center for intercompany loans. For example, consider a French subsidiary with excess cash that is needed by an affiliate in Italy. The treasury center CFC may intermediate the loan by borrowing from the French affiliate and lending to the Italian affiliate. The activities of the treasury center may cause it to be considered a dealer for U.S. tax purposes, which will result in its loan (the cash loan to the Italian affiliate) being marked to market. However, current regulations do not permit liabilities (here, the cash being borrowed from the French entity) to be marked to market. While some taxpayers believe that the borrowing is a short-position, there is uncertainty.

A third situation is that in which a CFC seeks to hedge its investment in the stock of another CFC. These hedges are commonly referred to as “net investment hedges.” While these hedges often qualify as investment hedges under financial statement rules, they typically do not qualify as hedges under the applicable tax rules since the asset being hedged is a capital asset. A similar situation, perhaps more common, arises when the hedge is at the level of a U.S. parent company and the investment being hedged is the parent company’s stock in a CFC.

A fourth situation involves hedges of entities that are treated as disregarded entities under the check-the-box-regime of the Treasury Regulations.

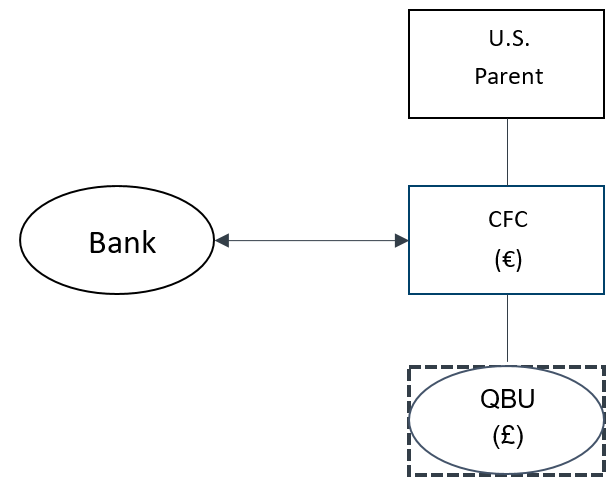

For example, consider a U.S. parent company that wholly owns a CFC that uses the euro as its functional currency. The CFC, in turn, wholly owns another entity (which has elected disregarded-entity status) that uses the British pound as its functional currency and operates a business that generates both subpart F and non-subpart F income. This disregarded entity is a qualified business unit (or “QBU”). This example illustrates the differences between the tax and accounting treatment of these hedges. The subsidiary using the British pound is a disregarded entity for U.S. tax purposes, but it is treated as a subsidiary for financial accounting purposes. Because the subsidiary using the British pound generated some subpart F income – if the intermediate CFC decided to hedge the currency risk of the QBU – the business needs exclusion would not be available. The result of these transactions is (i) the inclusion in the parent’s income (as subpart F income) of any foreign currency gain on the hedge, even though the underlying transactions (the business operations of the QBU) would have generated some non-subpart F income that would not be currently included in the U.S. parent’s income and (ii) if there were any losses on the underlying transactions, they would not reduce subpart F income.

This example illustrates the differences between the tax and accounting treatment of these hedges. The subsidiary using the British pound is a disregarded entity for U.S. tax purposes, but it is treated as a subsidiary for financial accounting purposes. Because the subsidiary using the British pound generated some subpart F income – if the intermediate CFC decided to hedge the currency risk of the QBU – the business needs exclusion would not be available. The result of these transactions is (i) the inclusion in the parent’s income (as subpart F income) of any foreign currency gain on the hedge, even though the underlying transactions (the business operations of the QBU) would have generated some non-subpart F income that would not be currently included in the U.S. parent’s income and (ii) if there were any losses on the underlying transactions, they would not reduce subpart F income.

The Proposed Regulations

The Proposed Regulations make a number of important changes. Overall, the changes are quite favorable to taxpayers.

First, they eliminate the cliff effect that might otherwise apply in analyzing the business needs exclusion. This means that the hedge will qualify for the business needs exclusion to the extent the gain relates to property that does not generate subpart F income. In other words, at least part of the hedge gain will not have to be currently included in income under subpart F. However, it is not totally clear whether aggregate hedges will be covered by these new rules. The Proposed Regulations refer to bona fide hedges of a “transaction,” as opposed to “transactions.” If the provision isn’t changed before the Proposed Regulations are finalized, this could leave open an argument that aggregate hedges of property (or net exposure from assets and liabilities) are excluded from the definition of “bona fide hedges.” The Proposed Regulations make it clear that the currency gain or loss on a “bona fide hedge” of an intercompany loan is apportioned between subpart F income and non-subpart F income in the same manner as the currency gain or loss on the loan. This creates symmetry between the loan and the related hedge.

Second, the Proposed Regulations permit taxpayers to elect to mark to market currency gain or loss, regardless of whether the foreign gain is on an asset or a liability. This is achieved through the addition of Proposed Treasury Regulation 1.988-7. The remeasurement of the currency gain or loss does not account for changes in interest rates or credit ratings, so it is not a true mark to market because it is not marked to fair market value. However, it is consistent with the remeasurement process under GAAP and helps resolve the treasury center mismatch issue described above. The Proposed Regulations also state that the acquisition of a debt instrument can be treated as a “bona fide hedge” of an interest-bearing liability.

Third, the Proposed Regulations allow application of the business needs exclusion to a net investment hedge in a foreign branch to the extent the gain is allocable to non-subpart F income. This type of hedge is referred to as a financial statement hedge. To qualify, the hedge must qualify under GAAP rules as a net investment hedge, the results of which are reflected in the cumulative translation account (“CTA”) associated with the QBU. If the position qualifies, the taxpayer then allocates the gain on the hedge to non-subpart F income in the same way it allocates section 987 gain (the proportion of assets that do and do not produce subpart F income).

Fourth, the IRS and the Treasury Department in the preamble to the Proposed Regulations request comments on whether the business needs exclusion should apply to hedges of a foreign-subsidiary corporation (in addition to foreign branches). The existing rules do not permit gains related to hedges of the stock of a CFC to qualify for the business needs exclusion because the business needs exclusion only applies to “ordinary property,” and stock in a corporation is never ordinary property for this purpose. The IRS and Treasury Department also request comment on whether the hedge of an intercompany loan to a disregarded entity qualifies for the business needs exclusion.

Open Issues

A few important issues remain under the Proposed Regulations.

Who Makes the Election? There is a question of who can make the election under Proposed Regulations section 1.988-7 – specifically, whether making the election for one subsidiary will affect the ability of another subsidiary to make the election. What if the subsidiaries are all disregarded entities for tax purposes?

Clarification of the Allocation Rule in the Business Needs Exclusion. There is a question about how to compute the amount of foreign currency gain or loss to allocate to non-subpart F income where there is foreign currency gain or loss because of a transaction from property that gives rise to (1) subpart F income (other than foreign currency gain or loss) and (2) non-subpart F income, or a bona fide hedging transaction with respect to such transaction or property, and it otherwise satisfies the requirements of the business needs exclusion.

Effective Date Issues. The Proposed Regulations suggest that a calendar year taxpayer could apply them to the 2017 tax year without consent. Yet, a question arises of what taxpayers should do if the Proposed Regulations are not finalized by the date their tax return is due. There have been conflicting public statements by Treasury officials on this issue. Many commentators believe that the election can be made in 2018 on a retroactive basis for years ending in 2017.

GILTI

One consequence of an effective election under the business needs exclusion is that the income that qualifies for the exclusion is not subpart F income. In such a case, the hedging income will be considered GILTI. GILTI generally captures all non-subpart F income and taxes it at a 10.5% rate. This means that, although the rate is more favorable under GILTI than when income is included in subpart F income, the tax deferral that existed before tax reform is now gone. Yet, because of the whipsaw potential, there is considerable value in identifying hedging transactions, even though the deferral associated with such hedging transactions is no longer available.